Keysight Technologies (KEYS)·Q1 2026 Earnings Summary

Keysight Crushes Q1, Surges 16% on AI-Driven Beat and Massive Guide Raise

February 23, 2026 · by Fintool AI Agent

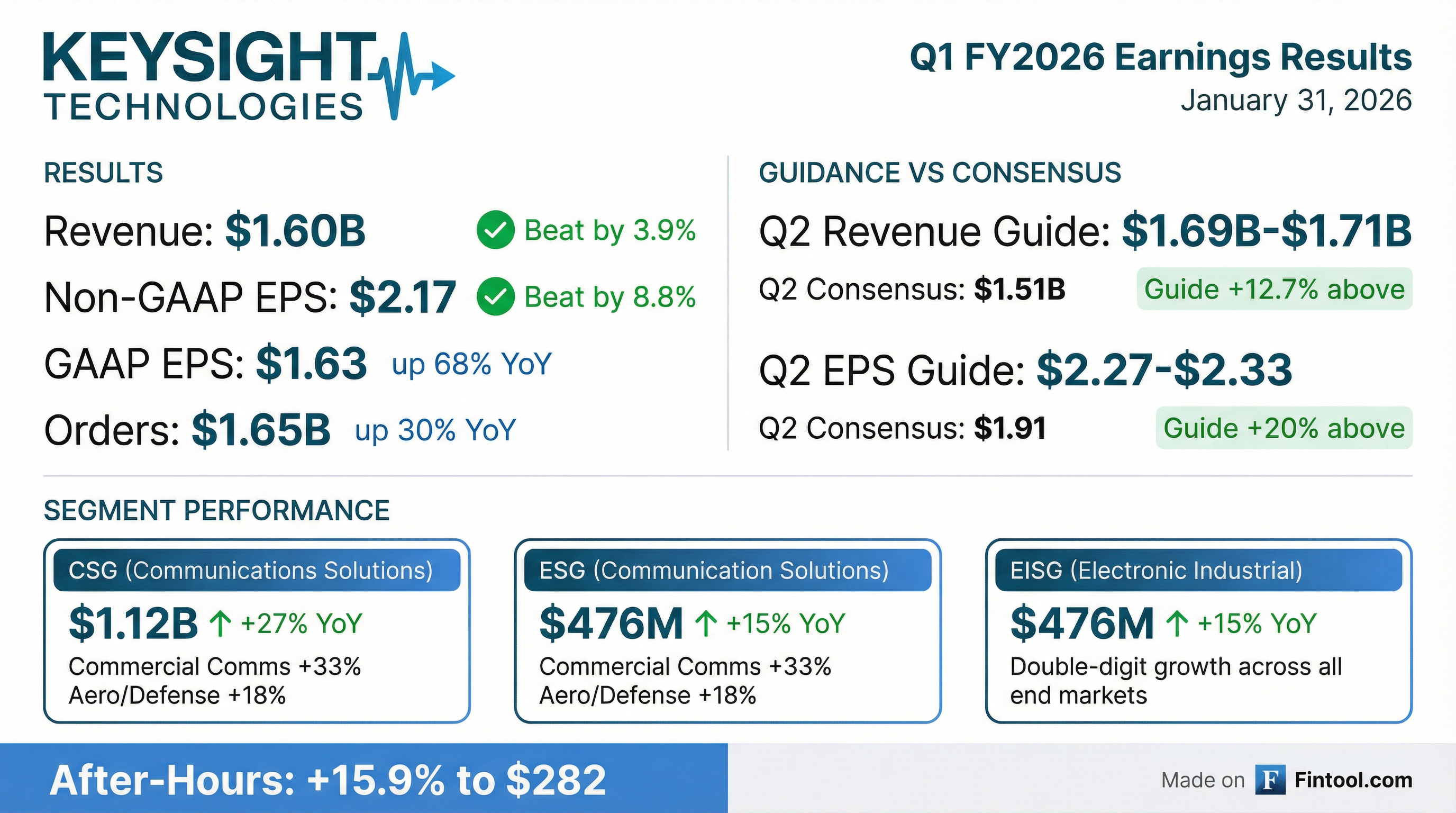

Keysight Technologies delivered a blowout Q1 FY2026, posting record revenue of $1.60 billion with double-digit growth across both segments as AI infrastructure demand continues to accelerate. The test and measurement leader beat consensus estimates by comfortable margins, then dropped an even bigger surprise with Q2 guidance that came in 13-20% above Street expectations. Shares surged nearly 16% in after-hours trading.

Did Keysight Beat Earnings?

Double beat. Eighth consecutive quarter. Keysight exceeded expectations on both revenue and earnings, continuing its remarkable streak of outperformance:

*Values retrieved from S&P Global

Revenue growth of 23% YoY significantly accelerated from the 10% growth posted in Q4 FY2025, reflecting the compounding benefits of AI-driven wireline demand and successful integration of recent acquisitions.

What Did Management Guide?

Q2 guidance blew away expectations. This is where the real story is — Keysight's forward guidance came in dramatically above consensus, suggesting the beat-and-raise cycle has more room to run:

*Values retrieved from S&P Global

The midpoint of Q2 revenue guidance represents ~30% YoY growth, accelerating from Q1's already-strong 23%.

Full Year FY2026: Management raised the base case to "total annual revenue and earnings growth just above 20%" (on an all-in basis). CFO Neil Dougherty noted visibility is strong through Q3, with upside potential if Q1/Q2 momentum sustains.

Important caveat: Management explicitly noted guidance "does not contemplate any impact from the recently announced Supreme Court decision regarding tariffs, which we are still assessing."

How Did the Stock React?

+15.9% after-hours surge. KEYS closed the regular session at $243.54, then rocketed to $282.20 in after-hours trading — a move that would add roughly $6.5 billion to the company's market cap if sustained.

The stock has now more than doubled from its 52-week low, reflecting the market's re-rating of Keysight as a prime AI infrastructure beneficiary.

What Changed From Last Quarter?

Acceleration across all metrics. Q1 results showed meaningful improvement versus the already-strong Q4 FY2025:

The step-function improvement suggests Keysight's AI-related tailwinds are strengthening, not moderating.

Segment Performance Deep Dive

Communications Solutions Group (CSG): +27% YoY

Commercial communications growth of 33% reflects the continued buildout of AI data center infrastructure. Wireline delivered record orders, surpassing wireless for the first time, driven by demand for both R&D and manufacturing solutions. AI-related order growth was "significantly above" the company average of 30%, and AI revenue exposure (sized at ~10% of company revenue in Q4) is growing with robust momentum.

The aerospace & defense business posted 18% growth, benefiting from defense modernization spending and expanding opportunities with both traditional primes and emerging "neoprimes."

Electronic Industrial Solutions Group (EISG): +15% YoY

Notably, EISG achieved double-digit growth across all end markets. This is particularly significant for automotive, which had been a drag on results through much of FY2025 before stabilizing in Q4.

Key Management Commentary

CEO Satish Dhanasekaran struck an optimistic tone:

"Since our last earnings call, we have seen further acceleration in demand with robust growth across business segments and key regions... The investments we've made over the last three years have strengthened our portfolio, deepened our customer relationships, and prepared us to capitalize on this unprecedented time."

SVP of Global Sales Steve Yoon provided striking context on pipeline strength:

"This was the highest quarter ever, and excluding acquisitions, our second highest on record, which is unprecedented for a quarter one for Keysight. In my 36 years with the company, this is one of the strongest funnels I've ever seen across the four dimensions that I track — short-term funnel, long-term funnel, funnel intake, and funnel velocity."

Four Drivers Shaping AI Wireline Demand

Management outlined four fundamental forces driving sustained wireline growth (now 9 consecutive quarters):

-

AI Infrastructure Scaling — Hyperscalers and ecosystems investing in scale-up and scale-out architectures. Keysight's full-stack portfolio across electrical, optical, RF, and network protocol enables end-to-end validation.

-

Higher Speeds & Ethernet-Based Networking — 800G/1.6T optics with 3.2T in development. Move to Ethernet-based AI fabrics creating test opportunities. Arbitrary waveform generators and oscilloscopes enabling 448 Gb/s per lane.

-

Optical Interconnects Rising — Co-packaged optics, optical circuit switching, and silicon photonics gaining adoption. Keysight's tunable laser sources and polarization synthesizers provide metrology-grade measurements.

-

System-Level Validation — As AI clusters scale, workload emulation solutions help customers solve deployment challenges by emulating real AI workload and stress conditions.

Q&A Highlights

AI Customer Expansion

Q: How is the AI customer base evolving — same customers expanding or new ones? A: "We've doubled the number of customers present at that demand. Our top 2 customers are still non-AI customers, reflecting broadening of demand across the globe and applications." Neoclouds are emerging as a new customer segment. International expansion is accelerating, with more business in Southeast Asia manufacturing hubs versus a year ago when it was heavily US-concentrated.

Operating Leverage & Margins

Q: How should we think about incremental operating margin leverage? A: "We've designed our business model about delivering a 40% core leverage on growth that's in the mid-single digits or better. This quarter, we delivered 41% leverage on significantly higher growth while absorbing the impact of tariffs." Core operating margin was 28.9%, up 170bp YoY.

Aerospace & Defense Trajectory

Q: Is this the beginning of a trajectory or a new run rate for A&D? A: Two factors: (1) Q1 benefited from delayed FY2025 spend flowing through year-end; (2) Looking ahead, European defense spending is increasing, and US primes are investing more in organic R&D and capacity additions. "The breadth of our portfolio with Mars Science Lab, space, satellite, radar, now combined with PNT from Spirent, allows us to make a broader impact."

Scale-Up vs Scale-Out Opportunities

Q: When do scale-up opportunities materialize? A: "We're seeing opportunities in scale-up as well as scale-out. There's quite a bit of R&D activity around 1.6T, 448 Gb/s per lane, and 3.2T. We are seeing expansion in those areas. Scale-up and scale-out are opportunities for us in both R&D and manufacturing."

Why Now?

Q: Why are orders accelerating now specifically? A: "2025 was a year we built momentum in the business. Now what we're experiencing is broad-based demand across all our businesses and regions. For AI specifically, there's continuing R&D demand and manufacturing is becoming important. But also aerospace & defense was up, wireless was up, EISG was up."

Balance Sheet Strength

Keysight's financial position remains robust:

Cash generation improved significantly from Q4, with FCF of $407M representing a 118% increase sequentially. The company also has a $1.5 billion share repurchase authorization.

Revenue Mix: Software and services accounted for ~40% of Q1 revenue, with annual recurring revenue (ARR) at 29% of total mix. The R&D vs. manufacturing mix is currently "a little bit below 60% R&D" due to increased manufacturing opportunity in wireline/data center buildout.

Historical Beat/Miss Trend

Eight consecutive quarters of double beats. The magnitude of Q1 FY2026's beat and the accompanying stock reaction represent the largest positive surprise in this streak.

What to Watch Going Forward

Catalysts

- Q2 earnings execution — Can they deliver on the raised guidance?

- Acquisition integration — Spirent, Optical Solutions Group, and PowerArtist contribute ~$375M FY2026 revenue

- 6G early design wins — Management noted the industry is "shifting from pure research to early pre-standards designs"

- Tariff resolution — Guidance excludes potential IEEPA tariff impacts

Risks

- AI capex cycle durability — Hyperscaler spending remains the key demand driver

- Tariff uncertainty — February 20 Supreme Court ruling not yet reflected in guidance

- Acquisition dilution — Management guided for "mild" EPS dilution from recent deals in FY2026

- China exposure — Geopolitical tensions remain a headwind

The Bottom Line

Keysight delivered a statement quarter that validates its positioning as a primary beneficiary of AI infrastructure buildouts. With revenue accelerating to 23% growth, orders up 30%, and guidance dramatically above consensus, the test and measurement leader is firing on all cylinders. The 16% after-hours pop reflects the market recognizing this isn't just a beat — it's confirmation of a structural growth inflection.

The key question now is sustainability. If Q2 results match the guidance trajectory, Keysight's stock re-rating likely has further to run. The tariff wildcard introduces near-term uncertainty, but management's track record of execution — eight straight double beats — earns them benefit of the doubt.

Related: Keysight Company Overview | Q4 2025 Earnings Transcript